Inside Super #3

The forces at work in retirement: a call to action for Australia’s super funds

In this issue of Inside Super we discuss how super funds can lead in retirement.

Profit-to-member funds have doubled their share of Australia’s retirement market in the past 8 years, but achieving leadership by 2030 will require innovation, policy reform and coordinated action. With drawdown assets surging, an ageing population, and rising member expectations, super funds must evolve from a savings model to a retirement income system, focusing on seamless experiences, personalised guidance, strong investment performance, and proactive policy engagement.

Last year, our Forces at Work Report (2024 edition) carried the headline Maximising Members’ Retirement Outcomes. The subheading captured a remarkable achievement, and an urgent challenge:

Profit-to-member funds double retirement market share in 8 years, but significant challenges must be met to achieve market leadership by 2030.

This doubling of market share was just one of several striking findings from the Report. Consider these key facts:

- ·Assets in drawdown were projected to grow from $722 billion in FY2023 to $4 trillion by 2063, by which time drawdowns are expected to almost match contributions.

- Between 2020 and 2024, industry and public sector funds overtook retail funds by share of member assets (not yet member accounts) in drawdown, translating accumulation-phase success into the retirement phase.

- Just 14 profit-to-member and retail funds held 80% of all drawdown accounts and assets.

- Profit-to-member funds occupied 3 of the top 5 spots for share of drawdown assets.

- On average, profit-to-member funds had higher drawdown balances than the retail sector.

- Account-based pensions represented approximately 84% of drawdown assets.

- ·Workforce participation among older Australians had roughly doubled since the early 1990s.

- In 2024, there were 6 times as many mortgage holders aged 55+ as there were in the late 1990s.

- ·Nearly half of Australian renters over 65 were living below the poverty line in FY2020.

Retirement: still front and centre

Of the 4 chapters in last year’s Report, 3 focused on retirement. This year’s Report (2025 edition) re-examines industry structure, competition and performance – the staples of this annual publication for more than a decade – but it also probes the strategic battlegrounds of an increasingly concentrated market, the significance of Australia’s superannuation system and bridging the advice gap.

At its heart, Forces at Work is about the big shifts shaping superannuation – and today, those shifts are inseparable from retirement outcomes. Older Australians are becoming a larger share of the population, and superannuation is playing a bigger role as a source of income in later life.

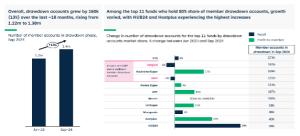

Recent data shows drawdown accounts continue to grow, now totalling 1.4 million. Eleven profit-to-member and retail funds control more than 80% of all drawdown assets, down from 14 the previous year. Among the leaders, all but two (Insignia and AMP) are growing their market share of drawdown accounts.

The number of drawdown accounts has been on the rise over the last 18 months, reaching 1.4m, with positive growth results for the top super funds by market share except for Insignia and AMP

Note: “Drawdown refers to transition to retirement (TTR) and retirement pension products. Defined benefit product are excluded. Retail funds have been aggregated up to their parent company/brands. To avoid distortions in 2024 due to successor fund transfers (SFTs), member accounts from merged funds have been included in the 2023 totals of the surviving funds.

Source: APRA. (2024, December). Quarterly Superannuation Product Statistics. September 2024. Table 1a; Right Lane Consulting. (2025).

A small number of profit-to-member funds are outperforming peers in the drawdown phase compared with accumulation.

Within the profit-to-member sector, a few funds outperform in drawdown compared to accumulation, with Equip Super among the ‘Big 8 in retirement’

¹The largest 12 funds: by market share of member assets in drawdown phase have been shown on this chart.

Note: ‘Drawdown’ refers to transition to retirement (TTR) and retirement pension products. Defined benefit products are excluded. Retail Funds have been aggregated up to their parent company brands

Sources: APRA. (2024, December). Quarterly Superannuation Product Statistics. September 2024. Table 1a.; Right Lane Consulting. (2025).

The innovation imperative — and the policy stalemate

Regulators and funds alike have identified product innovation as essential to better retirement offerings. In our most recent survey of Forces at Work Report subscribers, 60% said that providing members with a truly personalised retirement solution will require more than better service and engagement; it will demand genuine product innovation.

Yet uptake of new longevity products remains low. Treasury continues to push for stronger longevity protection, but consensus on a clear pathway remains elusive. It is worth recalling that as far back as 2016, Right Lane Consulting convened a cross-sector forum of leaders, regulators and experts to chart the future of retirement incomes. The priorities identified then – including boosting the level, stability and longevity of retirement income, and smoothing the transition from accumulation to drawdown – are as relevant today as they were nearly a decade ago.

From retirement savings to retirement income

The 2024 Report closed with a clear message: Australia’s super system, admired globally for its coverage and performance, must now evolve from a savings system to a genuine retirement income system. Funds told us that progress has been hampered by policy settings that remain complex and fragmented, creating operational friction for funds, partners and members alike. There is a pressing need to get the long-term settings right, and to design a system that works not just for those who are engaged, financially literate or well-advised, but for all Australians.

Winning in retirement: what it takes

For super funds, retirement is mission-critical. The demographic reality is clear: older Australians are living longer, and their financial wellbeing is increasingly shaped by the performance of their superannuation in retirement.

Funds must respond to a convergence of factors: an ageing population and longevity risk, shifting regulation, evolving investment and liquidity considerations, and rising member expectations. Right Lane Consulting has identified 6 attributes of funds that will lead in retirement:

- A seamless member experience

- Trusted guidance at scale

- A data-driven personalisation engine

- Leading investment performance

- A reliable and efficient payments service

- An active role shaping and responding to policy.

Lifting retirement outcomes will demand coordinated action – within funds, across the sector, and in partnership with policymakers. Decisive steps are needed without delay.

We suggest that funds use the 6 attributes listed above as a diagnostic tool, and consider their responses to the following additional points/questions:

- Leading funds aren’t waiting for perfect policy settings. For example, UniSuper is rolling out a digital advice engine, aimed at ‘missing middle’ members who typically forego financial advice, which begins with accumulation choices and will soon span contributions, insurance and pension drawdowns; so, much of the groundwork is done for full retirement advice delivered digitally, the day policy regulation allows for it. Is your fund doing everything it can to maximise your retirement proposition within the current policy settings?

- Many retirees’ journeys are no longer linear. A growing share of members work beyond preservation age, return to the workforce, or supplement retirement income through multiple sources. These shifting realities can challenge the assumptions behind traditional segmentation models, retirement products and advice pathways, requiring more flexible solutions. Does your fund meet the unique needs of members with non-traditional retirement paths?

- As profit-to-member funds strengthen their market positions in the drawdown phase, scale and strong data capabilities create opportunities to personalise the retirement income experience. Is your fund fully leveraging scale and data capabilities to deliver compelling retirement income solutions? Is your fund seeking to deliver differentiated solutions and more broad-based approaches that you expect to meet the needs of most members in drawdown? Has your fund struck the right balance?

We hope you find these insights useful. Please send me any feedback and if you would like I can publish it with the next issue, attributed or not, as you wish.

About Inside Super

The focus of Inside Super is on superannuation industry strategy, structure, scale economies, competition and growth – topics central to the work Right Lane has been doing for more than 25 years. We won’t be building the content from scratch. We’ve been writing about forces at work in the industry for 13 years in our annual, subscriber-only Forces at Work in Super Report.

In each issue, I choose a chart or two from the back issues of the Report (there’s ~1,100 pages to draw from!), and connect them up with something that’s happening right now in, for example, the competitive arena or the policy discourse. I also make some observations and suggest some questions you and your team should contemplate.

With the 2025 Forces at Work Report having been recently released, we are in presentation mode. If you are wondering whether your organisation is a subscriber, and if so whether you can get a copy, or if you would like us to present some of the Report findings to your team, please let me know.

I plan on writing editions of Inside Super semi frequently. If you do not wish to receive these updates, please let me know via return email and I will take you off the list.