Inside Super 6 | The structural squeeze on super funds

The 2026 Forces at Work Report (14th edition) is out.

It focuses on the structural squeeze on super funds. With scale largely secured, structural cost pressures, demographic headwinds and intensifying competition for members are reshaping the system’s economics, while operating more design is emerging as an increasingly important driver of performance.

If your organisation is a subscriber, and you haven’t yet received it, it’s in the inbox of one of your senior colleagues. If you are not sure, please email me.

Each year, once the Report is released, I review it through a sub-editor’s lens to identify media-worthy stories. This year, 5 stood out. I’ve outlined them in this issue of Inside Super, alongside supporting charts from the Report and a few ‘so whats’.

As an incentive to read to the end, I’ve included a value creation framework for AI in super.

Story 1: Advisors strike back: the battle for member trust

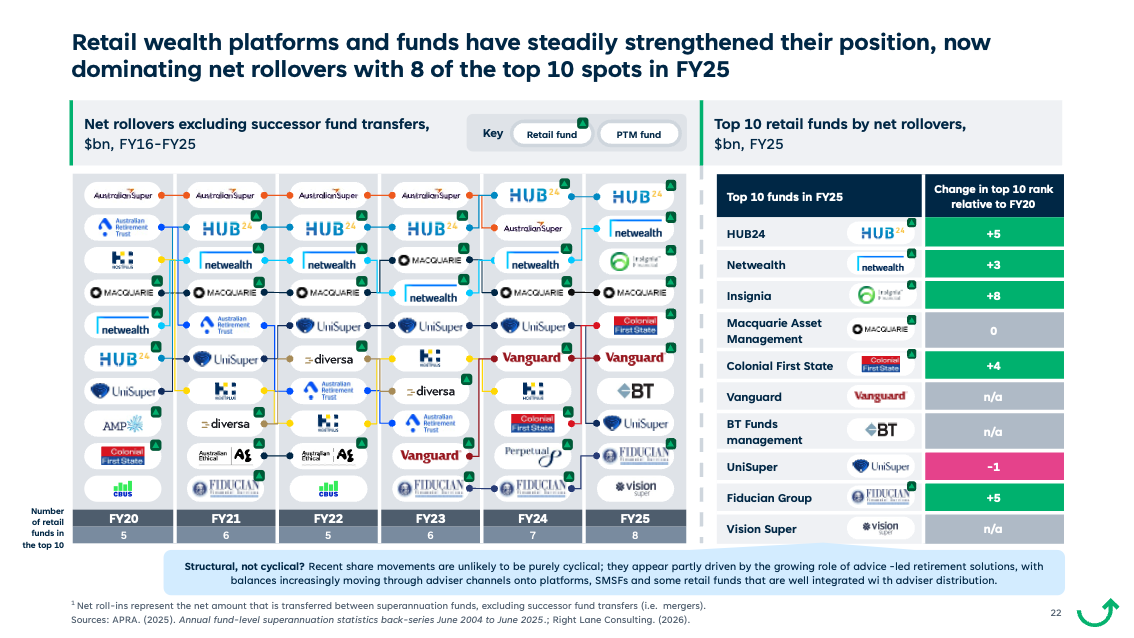

One of the ‘longitudinal’ stories in the Report’s recent editions has been the change in market share winners. In the 7 years to FY2023, a handful of large industry funds won nearly $70bn of market share (switching or competitive flows). This was a trend on foot before and exacerbated by the Hayne Royal Commission. In the last 2 years, that trend has reversed, with retail, notably advisor centric platforms, winning market share. As the following chart from the Report shows, 8 of the top 10 market share winners were from the for-profit sector in FY2025.

A major sub-plot to this story is the success of advisors and the platforms that have enabled their success, including Hub24 and Netwealth. Evidence suggests that as the super system matures and assets concentrate among higher-balance members approaching retirement, advice-led portfolio implementation through platforms is playing an increasingly important role in shaping competitive switching flows.

We suggest funds ‘fight back’ via 3 strategies, which we expound in the Report: strengthen mechanisms supporting member decision-making; use behavioural design, segmentation and proactive engagement (particularly at key life stages); and build strategies to participate in adviser-led distribution.

Story 2: Cashing out sooner: the new risk for super funds

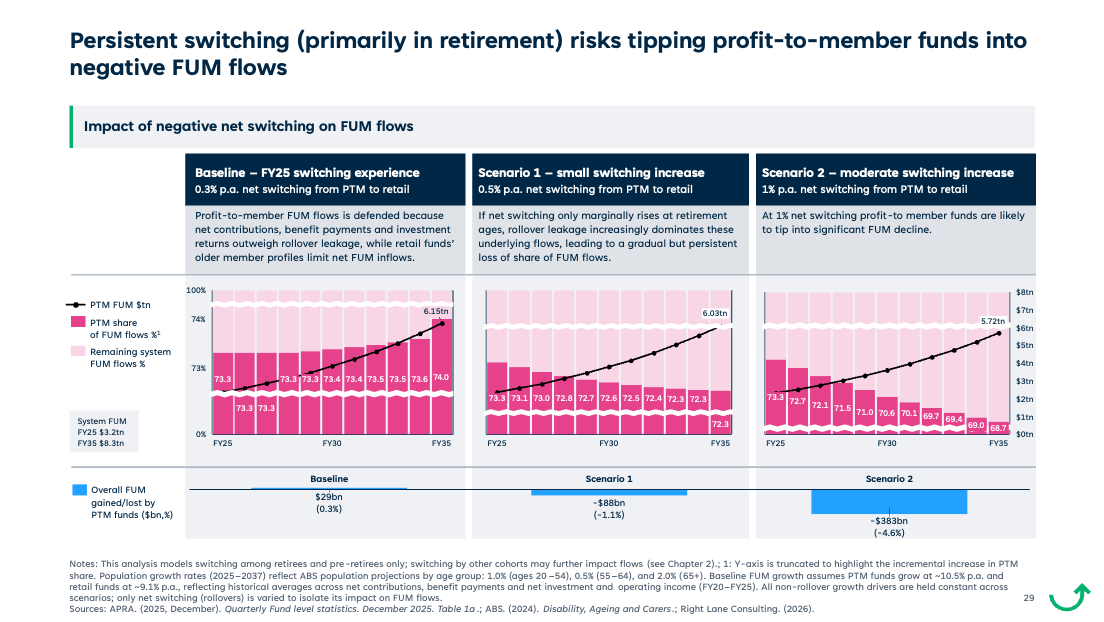

Older Australians are making up a growing share of the population and super is becoming an increasingly significant source of income in retirement. Getting retirement ‘right’ is critical to profit-to-member fund sustainability – even small increases in member leakage at retirement will materially impact FUM flows over time.

The adviser and platform-led channel is expected to be the leading growth driver over the next decade, overtaking employer and brand-led acquisition. As balances rise and super becomes an increasingly important asset, members are relying more heavily on advisers, who are increasingly directing assets onto adviser-centric platforms. As shown in the following chart from the Report, persistent retirement leakage risks are tipping profit-to-member funds into negative FUM flows.

Drawing on the 2024 Forces at Work Report, our recent work and discussions with industry leaders, Right Lane has identified 6 attributes of ‘winning in retirement’, including shaping and responding to policy, a data-driven personalisation engine and a reliable payments service. The Report includes 3 retirement case studies, which illustrate how funds are pursuing different pathways to success, with ‘trusted guidance at scale’ emerging as a common aspiration.

Story 3: Cut costs, lift service: the super balancing act

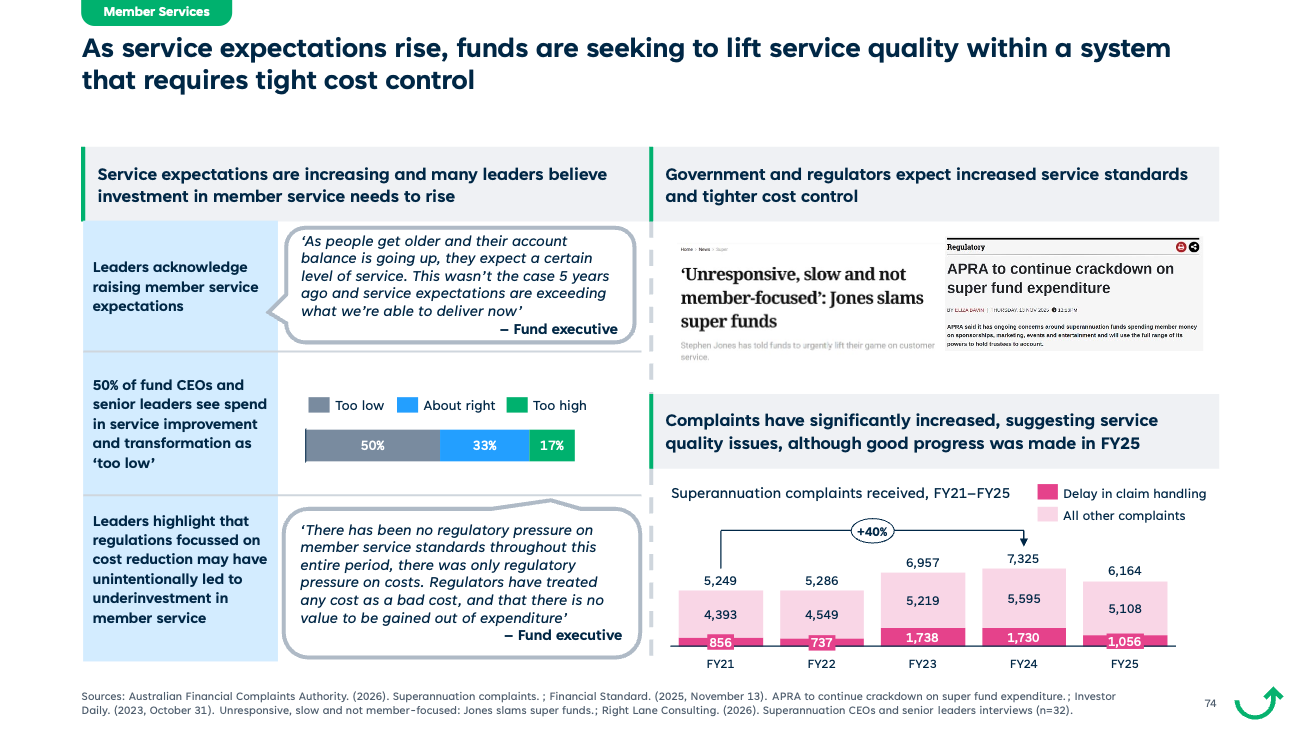

The super system has entered a new cost environment. For example, operating cost pressures have accelerated for profit-to-member funds, rising ~3.2× faster than members in 2019-25. Leaders no longer expect to naturally capture scale benefits. Instead, the prevailing view is that cost pressure is structural and problematic.

The chart below suggests that funds are seeking to improve member service; but they are doing so against a backdrop of cost control. Half the leaders we spoke with believe that spending on service improvement and transformation is too low, with some suggesting that regulatory pressures have unintentionally resulted in underinvestment in member service.

In the Report, we put forward the view that the next phase for super funds requires ‘cost-by-design’, not cost containment per se. This involves explicitly linking spend to member outcomes, providing visibility on cost drivers for decision making, and simplifying where complexity does not ‘earn its keep’. Ultimately, funds that can design their operating model so that spending consistently converts into demonstrable member value will be best placed to sustain trust, meet regulatory expectations and maintain long-term strategic advantage.

Story 4: A 3-track future for super fund growth

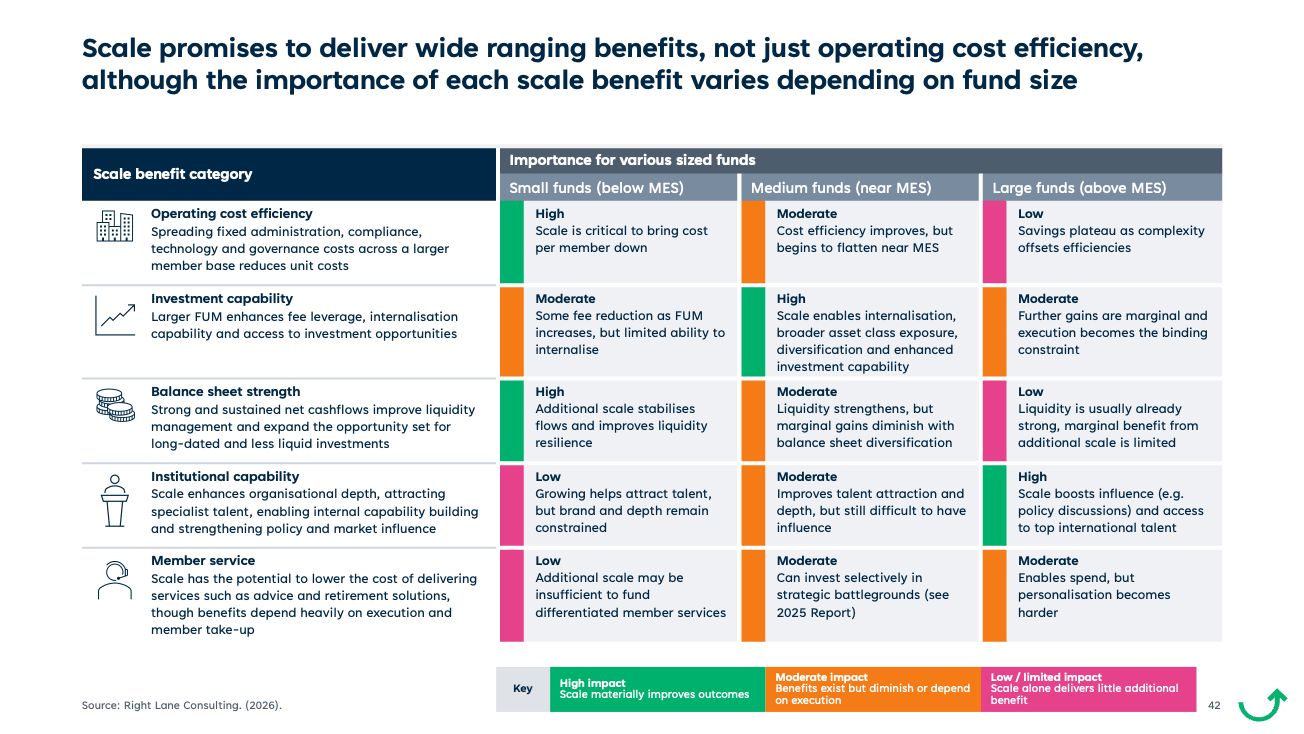

Historically, the main imperative for growth was reaching minimum efficient scale (MES), the point at which incremental scale began to deliver limited additional operating cost efficiencies. Right Lane was the first to propagate this notion in profit-to-member super, in the 2010s.

In 2026, most accounts in profit-to-member funds are with a fund that is well above the minimum efficient scale. However, in the last 5 years the operating cost curve has pushed outwards. For most funds, these cost increases have more than offset scale benefits captured from growth.

We now think about growth and scale benefits more broadly, including greater investment capability, balance sheet strength, enhanced institutional capability and improved member service. Scale delivers different benefits to different sized funds, as shown in the following chart from the Report.

Broadly speaking, the growth playbook is unchanged for smaller funds, increasingly targeted for medium funds, and a strategic choice for large funds. Growth initiatives should not be assessed on scale alone, but on whether existing members are better off, considering both potential benefits and costs. Five capabilities stand out for larger funds: strategic growth discipline, competitive flow capture, member lifetime value maximisation, complexity and integration management and selective capital deployment.

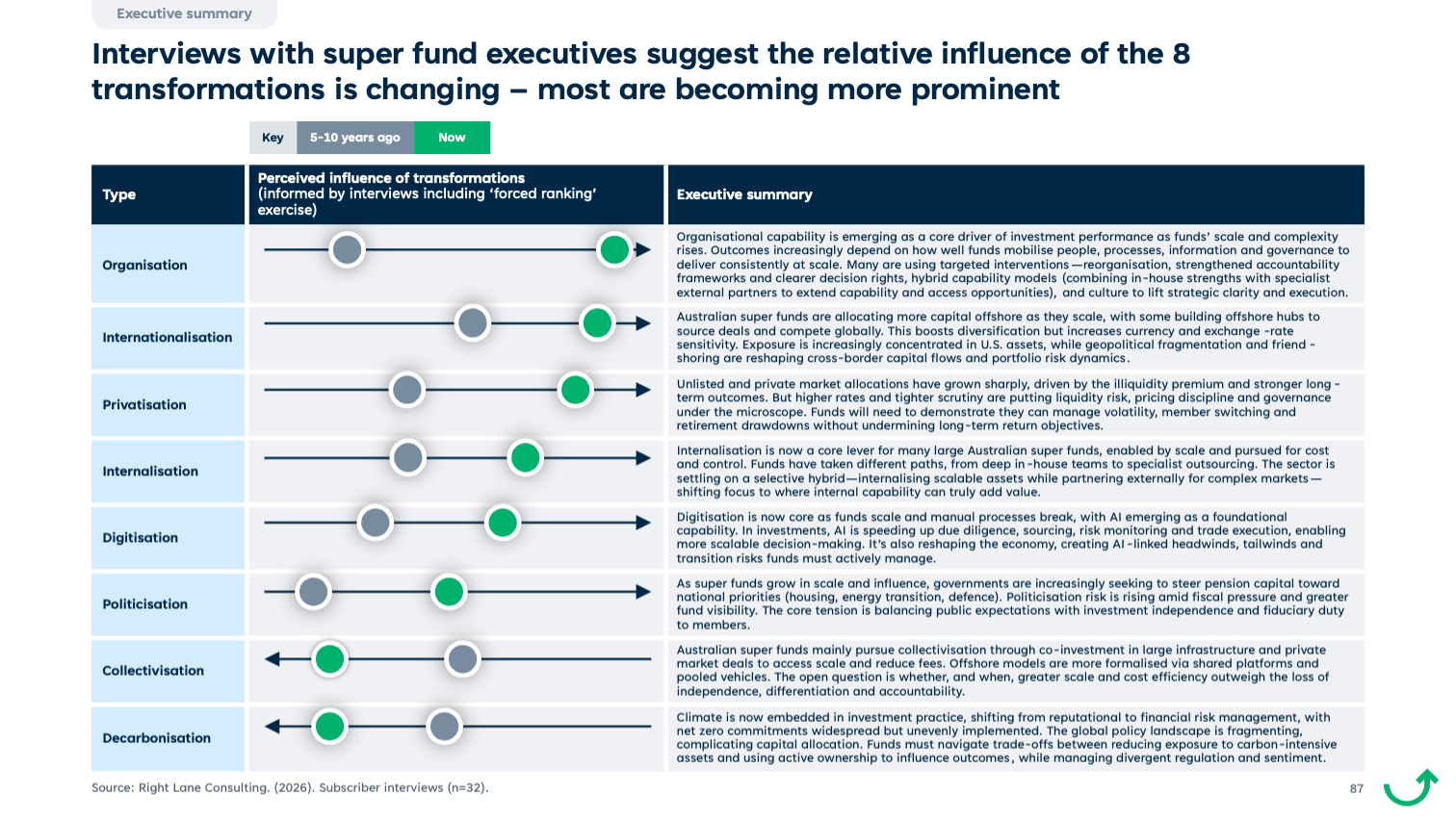

Story 5: The 8 transformations of institutional capital

Eight structural transformations are reshaping institutional capital, with their relative influence continuing to evolve. Internationalisation, privatisation, internalisation and digitisation (including AI) continue to be core drivers of performance and capability at scale for some. Decarbonisation and collectivisation remain embedded in strategy, though momentum and emphasis have become more nuanced. Politicisation is rising as funds become more visible and face pressure to align capital with national priorities. As shown in the following chart, organisation stands out as a critical lever of sustained investment performance.

Interviewees consistently rated organisational capability as the highest-impact transformation for improving funds’ net investment performance. Interviewees and analysis pointed to 4 practical levers: strategic reorganisation, decision-making alignment, hybrid enterprise capability models and culture. Together, these interventions aim to improve clarity, speed and scalability of investment delivery while reinforcing accountability and long-term discipline.

Bonus: Value creation framework for AI in super

In the introduction to this issue of Inside Super, I promised a way of thinking about the value super funds are getting from their AI experiments. I believe that as they contemplate AI investments, funds should start with a value driver tree like the one below, attach clear quantitative value metrics to each branch and take a top-down approach to value creation.

This is quite different from how AI is often pursued today, through bottom-up, disconnected experiments with limited visibility on how they create value.

Instead, we suggest that funds use the value driver tree to guide their AI efforts, asking:

- How do our AI initiatives map to each branch of the tree?

- If we execute this portfolio of initiatives, will we actually deliver the value outcomes we’re targeting?

- If not, which areas do we need to dial up or invest in further?

This approach creates discipline. It helps to ensure that AI efforts are anchored in member value, not just technical possibility. It also provides a clear line of sight from individual experiments to enterprise outcomes, showing how each initiative contributes to overall member value, rather than operating as an isolated activity.

Indicative AI and automation value creation framework

About Inside Super

The focus of Inside Super is on superannuation industry strategy, structure, scale economies, competition and growth – topics central to the work Right Lane has been doing for more than 25 years. We won’t be building the content from scratch. We’ve been writing about forces at work in the industry for 13 years in our annual, subscriber-only Forces at Work in Super Report.

In each issue, I choose a chart or two from the back issues of the Report (there’s ~1,100 pages to draw from!), and connect them up with something that’s happening right now in, for example, the competitive arena or the policy discourse. I also make some observations and suggest some questions you and your team should contemplate.

With the 2025 Forces at Work Report having been recently released, we are in presentation mode. If you are wondering whether your organisation is a subscriber, and if so whether you can get a copy, or if you would like us to present some of the Report findings to your team, please let me know.

I plan on writing editions of Inside Super semi frequently. If you do not wish to receive these updates, please let me know via return email and I will take you off the list.